Credit is crucial in the US. Renting an apartment or borrowing money to buy a house is challenging if you have no credit or bad credit. Your credit score determines your eligibility for loans and credit cards and affects the interest rate you get.

Despite how crucial credit is, there are many false myths. In this article, we debunk these myths and share 17 things you can do now that will actually improve your credit.

Related article: Why Credit Matters And The Best Advice That Will Make Credit Work For You

The Truth About Common Credit Myths

Here are some of the most common myths about credit:

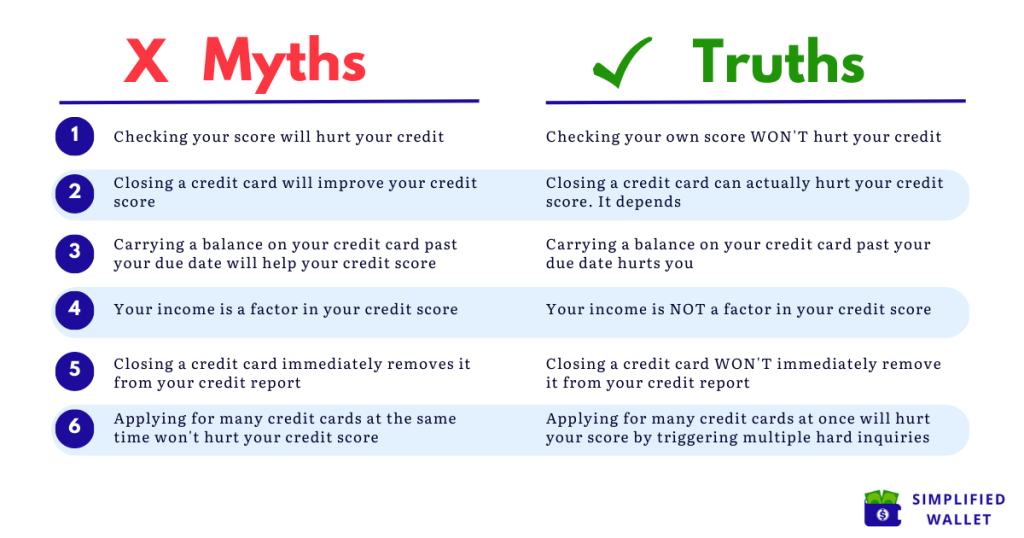

1) Myth: Checking your credit score will hurt your credit

Truth: Checking your own credit score will not hurt your credit. This is a “soft inquiry” and does not affect your credit score. Most credit card companies display your credit score when you log in to your account. You can check your score as much as you like. However, when you apply for new credit and a lender checks your credit score, this is a “hard inquiry” and can temporarily lower your credit score.

2) Myth: Closing a credit card will improve your credit score

Truth: Closing a credit card could hurt your credit score. It depends. It will hurt your score if it increases your credit utilization ratio or shortens your credit history. Your credit utilization ratio is how much credit you use compared to how much you have available. You want your utilization ratio to be as low as possible and never higher than 30%.

Imagine you have three credit cards:

-

- Blue card – $5,000 credit limit – opened in 2020

- Green card – $3,000 credit limit – opened in 2015

- Red card – $2,000 credit limit – opened in 2010

- Total available credit – $10,000

Suppose you spend $2,500 of your available credit across your three cards monthly. Your credit utilization ratio is 25% ($2,500/$10,000).

If you close your red card, your total available credit goes from $10,000 to $8,000. If you continue spending $2,500 monthly across your 2 remaining cards, your utilization ratio goes from 25% to 31.25%. You are now over 30%, which will lower your credit score. Also, you closed the red card, your oldest card. This shortens your credit history and will lower your credit score.

3) Myth: Carrying a balance past your due date will help your credit score

Truth: Carrying a balance on your credit card past your due date hurts you in two ways. One, you pay expensive credit card interest charges. These can range from 16% to 25% annually. Two, you increase your credit utilization ratio – the more of your available credit you use, the higher your utilization ratio and the lower your credit score.

Paying your credit card balance in full and on time each month improves your credit score. The most crucial factor in building credit is on-time payments. I always pay off my balance in full after my billing cycle ends, and my credit score is over 800.

4) Myth: Your income is a factor in your credit score

Truth: Your income is not a factor in your credit score. Your credit score is based on your payment history, credit utilization, length of credit history, and other factors related to how you use credit.

5) Myth: Closing a credit card immediately removes it from your credit report

Truth: Closing a credit card will not immediately remove it from your credit report. Closed accounts remain on your credit report for up to 10 years and may still impact your score during that time.

6) Myth: Applying for many credit cards at the same time won’t hurt your credit score

Truth: Applying for many credit cards at once will hurt your credit score by triggering multiple hard inquiries. While credit bureaus do not penalize you for applying for multiple mortgages simultaneously, it’s not the same for credit cards. The credit bureaus know you want to find the best mortgage terms. They treat multiple hard inquiries from different lenders within 14 to 45 days as one inquiry (The number of days depends on the credit scoring model used. Safest to use 14 days as a rule of thumb). However, this doesn’t apply to credit cards. All new hard inquiries for credit cards will lower your credit score individually.

Now that you know the truth about credit, you can take action to improve your credit score.

17 Things To Do Now That Will Actually Improve Your Credit Score

Do you have no credit history and need to apply for your first credit card? Have you struggled with credit and need to improve your credit score? Or are you planning to buy a house or a car soon and want a higher credit score to lower your interest rate? Whatever the reason, we’ve got you covered. Try at least one of our 17 things to do now to improve your credit score:

1) Get a regular or secured credit card

Credit cards offer an easy way to establish a credit history. You can apply and get a decision in a few minutes. You can choose the credit card that will work for you based on your credit score and preferred rewards. For example, I travel a lot, so I have the Chase Sapphire Reserve card to maximize my travel benefits.

You can get a secured credit card if you have bad credit or no credit. With a secured credit card, you provide money upfront as a deposit. However much you provide becomes your credit limit. Most secured credit cards require a minimum deposit of $200 to $300. Pick an amount you are comfortable with, as your deposit will be held until your card switches from a secured to a regular credit card. It can take 6 to 18 months for this to happen, depending on your financial habits.

I applied for my first credit card when I got my first job after college. I got rejected because I had no credit history. So I applied for a secured credit card instead. After 6 months, I now had a credit history and a credit score of 750. My card was converted to a regular card, and I got my deposit back.

2) Monitor your score

It’s tough to improve what you don’t measure. Check your credit score at least once a month and your credit report at least once a year. You can check your credit report for free each year. If you have a credit card, you can also check your credit score and credit report by logging into your account.

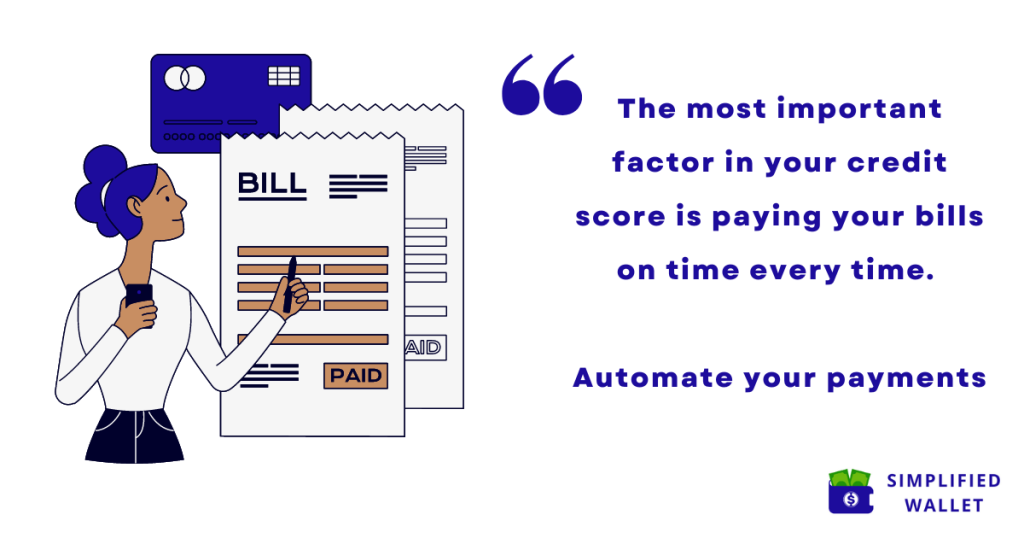

3) Automate your payments or set reminders

The most important factor in your credit score is your payment history. You want to make every payment on time every time. I recommend automating your payments. This ensures you will never miss a payment. You can do this for your credit cards, mortgage, student loans, phone bills, or car loans. You can pay the minimum, a fixed amount, or the entire balance automatically for credit cards. I recommend paying the full amount to avoid expensive interest fees. If you are hesitant to automate your payments, try it for 1 month and see how you feel. If you decide not to automate your payments, try setting a reminder on your calendar or an alarm on your phone. When it goes off, stop what you are doing and make your payment. It’s easy to get sidetracked and forget if you wait to do it.

4) Keep your credit utilization ratio under 30%

One of the fastest ways to improve your credit score is to improve your credit utilization ratio. Use as little as possible of your available credit, and never use more than 30%.

5) Ask for credit limit increases

Another way to improve your credit utilization ratio is to increase your credit limit. For example, if you have a $10,000 credit limit and use $3,000, your credit utilization ratio is 30% ($3,000/$10,000). If you ask for a credit increase and your limit becomes $15,000, you can still spend $3,000. But now your credit utilization ratio is 20% ($3,000/$15,000). You’ve lowered your utilization ratio and improved your credit score without changing your spending. The key is to keep your spending the same when you increase your credit limit. You can ask your credit card company to increase your limit roughly every 6 months. Some credit cards automatically increase your limit, but you don’t need to wait for this. You can log into your account and request a credit limit increase or call your credit card company.

6) Set balance alerts on your credit card

Are you finding it difficult to control your credit card spending? You can set balance alerts so you know when you are getting close to 10% or 30% of your limit. I set balance alerts for all three of my credit cards. I set alerts for when I spend more than $100 and for when my balance hits specific amounts like $1000 or $2500. When I see the alert, it forces me to stop and think about how much I’m spending that month.

7) Pay off some of your balance before the end of your billing cycle

Have you spent more than 30% of your credit limit? Did you know you can make early payments on your credit card? Most credit card companies report your balance after the end of your billing cycle. You can take advantage of this and pay off your balance before it gets reported to improve your credit utilization ratio and score. For example, if you spent $4,000 with a credit limit of $10,000 and your billing cycle is from April 10 to May 9, you can pay $3,000 on May 1 before your billing cycle ends. On May 9, when your credit card reports your balance, it will report it as $1,000. Pay off some but not all of it early.

8) Keep your oldest account open

The length of your credit history matters. Keep your oldest account open and use it even if it’s no longer your main account. For instance, I put my streaming subscription on my oldest credit card. It’s the only transaction on that card each month, but it keeps that account active, and I know that I’ll always be able to pay off the balance in full.

9) Freeze your credit

Cyber attacks and data breaches have increased. Protect yourself by freezing your credit. When your credit is frozen, no new accounts can be opened in your name. I have my credit permanently frozen to protect myself. It also makes me think twice before applying for new credit. To apply for new credit, I need to contact each of the three major credit bureaus to temporarily unfreeze my account. This forces me to only do this when it’s essential.

10) Space out new applications by at least 6 months

Too many new credit applications in a short time negatively affect your credit score. Space out new applications by at least 6 months. The only exception is when you are rate shopping for mortgages or car loans. Then it’s okay to apply for multiple mortgages to compare rates.

11) Pay off higher-interest debt first

Some financial institutions charge you interest on your interest. Your debt can quickly grow to unmanageable levels. Pay off higher-interest debt first to reduce how much interest you pay long-term across all your debt.

12) Pay off delinquent accounts first

The longer it takes to make a late payment, the more it affects your credit score. Pay down any delinquent accounts first while paying at least the minimum on your current accounts.

13) Renegotiate debt

Be proactive. You may be surprised at how helpful some financial institutions or government programs can be if you are struggling to pay off your debts. The pandemic and high inflation have added significant financial pressures to most Americans. The Consumer Financial Protection Bureau is a US government agency that ensures you are treated fairly by financial institutions. It has regularly updated information on programs to help you with medical bills, student loans, and mortgages. If you have a hard time making ends meet, there are government programs to help.

14) Refinance debt

If you do not qualify for debt forgiveness or can’t renegotiate your debt, consider refinancing your debt. This means you take out new debt to pay off existing debt. When refinancing debt, you want to reduce interest rates or lower monthly payments. Do your research and pick an option that works for you. For example, if you have high-interest credit card debt, you may pay an interest rate of 20% or more. Refinancing with a personal loan or balance transfer credit card can lower your interest rate to 10% or less. This can save you hundreds or even thousands of dollars in interest over the life of the loan. However, some credit cards charge for balance transfers, and some personal loans come with fees. Be mindful of this and combine refinancing debt with a plan to pay off the debt so the fees you incur are less than what you save.

15) Be an authorized user on someone’s account or get a co-signer

Ask a friend or relative with good credit to make you an authorized user on their credit card. Or get a co-signer if you need to rent an apartment, finance a car, or buy a house and have no credit or bad credit. Remember that your co-signer will be financially liable if you default, so make sure you can afford your monthly payments.

16) Build better financial habits and let time pass

Negative remarks do not stay on your credit history forever. As time passes, the impact diminishes. Build good credit behaviors, and over time, your negative history will no longer matter. Negative remarks stay on your credit report for the following amount of time:

-

- Bankruptcy – 10 years for Chapter 7 and 7 years for Chapter 13

- Collection account – 7 years

- Late payments – 7 years

- Hard inquiries – 2 years

17) Get help from a non-profit credit counselor

Are you overwhelmed? Do you feel like you need help to get yourself out of debt? For some people, it helps to have an experienced credit counselor support you through this process. Be careful, as there are scams and predatory for-profit credit repair companies that do more harm than good. You can find reputable non-profit credit counselors through the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

Great tips. My credit score drops when I pay my balance to zero. Do you know why? My utilization rate when I carry a balance is always less than 2%.

Thanks for sharing your experience! It’s great to hear you’re already maintaining a low utilization rate. Keep up the good habit! 👏🏾

The most likely explanation is the timing of when you make your payment and when your credit card company reports your balance to the credit bureaus. You don’t want your balance to be reported as $0. This makes it look like you aren’t using the card. You want your utilization rate to be under 10% but not zero. Most credit card companies report your balance at the end of your billing cycle. You can ask your credit card company if you are not sure.

Pay your balance in full after your billing cycle ends and before/when your bill is due. The goal is not to carry a balance past your due date. You will have to pay interest fees then. It’s okay to pay off some of your balance early (before the end of the billing cycle) to reduce your utilization ratio but don’t pay all of it off.