Lifestyle inflation means increasing your spending as you make more money, often spending on things you will later regret or forget.

It’s tempting to spend more when you make more money. In fact, you should spend more if it will improve your quality of life. The key is to differentiate between spending that improves your quality of life and spending that doesn’t. Ask yourself:

-

- What matters most to me

- What did I buy last month that brought me the most joy?

- What did I buy last month that I now regret?

- How can I use my answers to align my spending with my personal and financial goals?

It is essential to align your spending to your financial goals, so you don’t screw over your future self for things your present self doesn’t value (it’s easy to spend impulsively on things we later realize we don’t need).

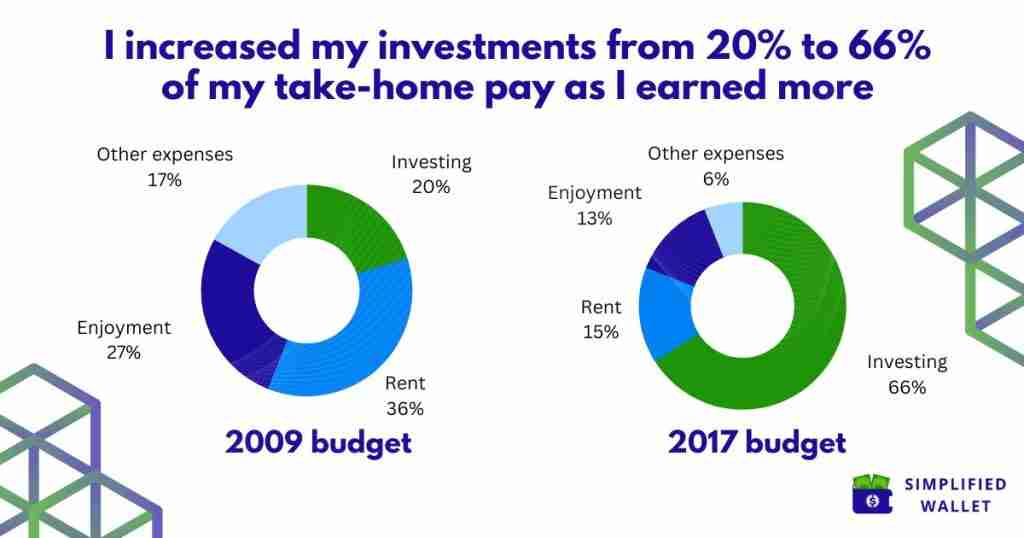

Back in 2009, I made $41,000 a year. After paying taxes, I spent ~$2,350 and invested $570 each month living in Washington, DC. I enjoyed my life – I went out to eat with friends, attended shows and concerts, and traveled to visit friends and family or explore new places.

In 2017, after graduating from business school, I made ~$150,000 a year. I spent $3,050 and invested $5,900 each month, still living in Washington, DC. I enjoyed my life doing the same things as in 2009 – shows, concerts, dining out, and travel. My spending increased by 30%, although my income was 3.6 times more. Instead of increasing my spending at the same rate as my income, I grew my investing by 10x.

Here are 4 strategies that helped me do this. If any resonate with you, try them and let me know if they help you avoid lifestyle inflation.

1) Understand what matters to you and align your spending to your values and financial goals

Our psychological needs influence our spending more than we think. In my 20s, I went to the mall and bought new clothes to cheer myself up if I had a bad week. Subconsciously I wanted to look good to feel good.

There’s nothing wrong with wanting to look good. However, it’s helpful to understand what truly matters to you and align your spending to your values and financial goals.

In 2017, I realized that family and friends mattered most to me, and I wanted more time with them. My goal is to invest enough money, so I have flexibility in what I do with my time. Whether that means taking a year off or working less hours.

To achieve this goal, I need to invest more money. Once I realized this, I was intentional about how I spent my money. I took out the money I needed to invest first. After that, I was free to spend whatever was left in my account on anything I wanted guilt-free. As my income grew from 2009 to 2017, I grew my investing from 20% to 66% of my take-home pay.

2) Enjoy your life

It’s much easier to save and invest consistently if you enjoy your life. I have an “enjoyment” bucket in my budget. Although I save and invest a large portion of my income, I also have a lot of fun, whether traveling to new countries, going on road trips with friends, or eating out at my favorite restaurants.

Related article: 49 Free Or Astonishingly Cheap Ideas To Have Fun When You Need To Spend Less

3) Focus on yourself and don’t compare yourself to others

We naturally compare ourselves to others. Sometimes, that’s a good thing. Seeing what others are doing can provide helpful insights. Role models and mentors shed light on how to achieve what you want.

However, comparing yourself to others can be destructive when you focus too much on what others have that you spend on what you can’t afford or you spend to the detriment of your financial future.

Everyone is on their own journey. You have different needs, goals, and preferences from everyone else. Only you know what you want for your life. When you keep your goals front and center, you can resist the temptation to “keep up with the Jones” and instead focus on achieving your personal and financial goals.

4) Save and invest more as your income grows

The more you save and invest, the faster you reach your financial goals. Whenever I got a raise, I increased my investments. First, I maxed out my 401K, then my IRA, and finally, I opened a brokerage account.

Each time I got paid, I invested. I automated my investments, so I didn’t have to think about it. I spent less than an hour a month investing from 2017 to 2021 as my net worth when from $26K to $1 million. My mantra is “Pay yourself first.”